We remember and honor those who gave all.

Source: KCM

We remember and honor those who gave all.

Source: KCM

There’s a lot of discussion about affordability as home prices continue to appreciate rapidly. Even though the most recent index on affordability from the National Association of Realtors (NAR) shows homes are more affordable today than the historical average, some still have concerns about whether or not it’s truly affordable to buy a home right now.

When addressing this topic, there are various measures of affordability to consider. However, very few of the indexes compare the affordability of owning a home to renting one. In a paper just published by the Urban Institute, Homeownership Is Affordable Housing, author Mike Loftin examines whether it’s more affordable to buy or rent. Here are some of the highlights included.

The report explains:

“When we look at the median housing expense ratio of all households, the typical homeowner household spends 16 percent of its income on housing while the typical renter household spends 26 percent. This is true, you might say, because people who own their own home must make more money than people who rent. But if we control for income, it is still more affordable to own a home than to rent housing, on average.”

Here’s the data from the report shown in a graph:

The report goes on to say:

“Buying a home is not a decision between investing in real estate versus investing in stocks, as financial advisers often claim. Instead, the home buying investment simply converts some portion of an existing expense (renting) into an investment in real estate.”

It explains that you still have a housing expense (rent payments) even if you don’t buy a home. You can’t live in your 401K, but you can transfer housing expenses to your real estate investment. A mortgage payment is forced savings; it goes toward building equity you will likely get back when you sell your home. There’s no return on your rent payments.

The report also notes:

“Whereas renters are continuously vulnerable to cost increases, rising home prices do not affect homeowners. Nobody rebuys the same home every year. For the homeowner with a fixed-rate mortgage, monthly payments increase only if property taxes and property insurance costs increase. The principal and interest portion of the payment, the largest portion, is fixed. Meanwhile, the renter’s entire payment is subject to inflation.

Consequently, over time, the homeowner’s and renter’s differing trajectories produce starkly different economic outcomes. Homeownership’s major affordability benefit is that it stabilizes what is likely the homeowner’s biggest monthly expense, assuming a buyer has a fixed-rate mortgage, which most American homeowners do. The only portion of the homeowner’s housing expenses that can increase is taxes and insurance. The principal and interest portion stays the same for 30 years.”

A mortgage payment remains about the same over the 30 years of the mortgage. Here’s what rents have done over the last 30 years:

As the report also indicates:

“We need to stop seeing housing as a reward for financial success and instead see it as a critical tool that can facilitate financial success. Affordable homeownership is not the capstone of economic well-being; it is the cornerstone.”

Homeownership is the first rung on the ladder of financial success for most households, as their home is most often their largest asset.

If the current headlines reporting a supposed drop-off in home affordability are making you nervous, let’s connect to go over the real insights into our area.

Source: KCM

The last year has put emphasis on the importance of one’s home. As a result, some renters are making the jump into homeownership while some homeowners are re-evaluating their current house and considering a move to one that better fits their current lifestyle. Understanding how housing affordability works and the main market factors that impact it may help those who are ready to buy a home narrow down the optimal window of time in which to make a purchase.

There are three main factors that go into determining how affordable homes are for buyers:

The National Association of Realtors (NAR) produces a Housing Affordability Index. It takes these three factors into account and determines an overall affordability score for housing. According to NAR, the index:

“…measures whether or not a typical family earns enough income to qualify for a mortgage loan on a typical home at the national and regional levels based on the most recent price and income data.”

Their methodology states:

“To interpret the indices, a value of 100 means that a family with the median income has exactly enough income to qualify for a mortgage on a median-priced home. An index above 100 signifies that family earning the median income has more than enough income to qualify for a mortgage loan on a median-priced home, assuming a 20 percent down payment.”

So, the higher the index, the more affordable it is to purchase a home. Here’s a graph of the index going back to 1990: The blue bar represents today’s affordability. We can see that homes are more affordable now than they’ve been at any point since the housing crash when distressed properties (foreclosures and short sales) dominated the market. Those properties were sold at large discounts not seen before in the housing market for almost one hundred years.

The blue bar represents today’s affordability. We can see that homes are more affordable now than they’ve been at any point since the housing crash when distressed properties (foreclosures and short sales) dominated the market. Those properties were sold at large discounts not seen before in the housing market for almost one hundred years.

Although there are three factors that drive the overall equation, the one that’s playing the largest part in today’s homebuying affordability is historically low mortgage rates. Based on this primary factor, we can see that it’s more affordable to buy a home today than at any time in the last eight years.

If you’re considering purchasing your first home or moving up to the one you’ve always hoped for, it’s important to understand how affordability plays into the overall cost of your home. With that in mind, buying while mortgage rates are as low as they are now may save you quite a bit of money over the life of your home loan.

If you feel ready to buy, purchasing a home this summer may save you a significant amount of money over time based on historical affordability trends. Let’s connect today to determine if now is the right time for you to make your move.

Source: KCM

As we enter the middle of 2021, many are wondering if we’ll see big changes in the housing market during the second half of this year. Here’s a look at what some experts have to say about key factors that will drive the industry and the economy forward in the months to come.

“. . . homes continue to sell quickly in what’s normally the fastest-moving time of the year. This is in contrast with 2020 when homes sold slower in the spring and fastest in September and October. While we expect fall to be competitive, this year’s seasonal pattern is likely to be more normal, with homes selling fastest from roughly now until mid-summer.”

“Sellers who have been hesitant to list homes as part of their personal health safety precautions may be more encouraged to list and show their homes with a population mostly vaccinated by the mid-year.”

“Surveys showed that seller confidence continued to rise in April. Extra confidence plus our recent survey finding that more homeowners than normal are planning to list their homes for sale in the next 12 months suggest that while we may not see an end to the sellers’ market, we might see the intensity of the competition diminish as buyers have more options to choose from.”

“We forecast that mortgage rates will continue to rise through the end of next year. We estimate the 30-year fixed mortgage rate will average 3.4% in the fourth quarter of 2021, rising to 3.8% in the fourth quarter of 2022.”

Experts are optimistic about the second half of the year. Let’s connect today to talk more about the conditions in our local market.

Source: KCM

Today’s housing market is full of unprecedented opportunities. High buyer demand paired with record-low housing inventory is creating the ultimate sellers’ market, which means it’s a fantastic time to sell your house. However, that doesn’t mean sellers are guaranteed success no matter what. There are still some key things to know so you can avoid costly mistakes and win big when you make a move.

When inventory is low, like it is in the current market, it’s common to think buyers will pay whatever we ask when setting a listing price. Believe it or not, that’s not always true. Even in a sellers’ market, listing your house for the right price will maximize the number of buyers that see your house. This creates the best environment for bidding wars, which in turn are more likely to increase the final sale price. A real estate professional is the best person to help you set the best price for your house so you can achieve your financial goals.

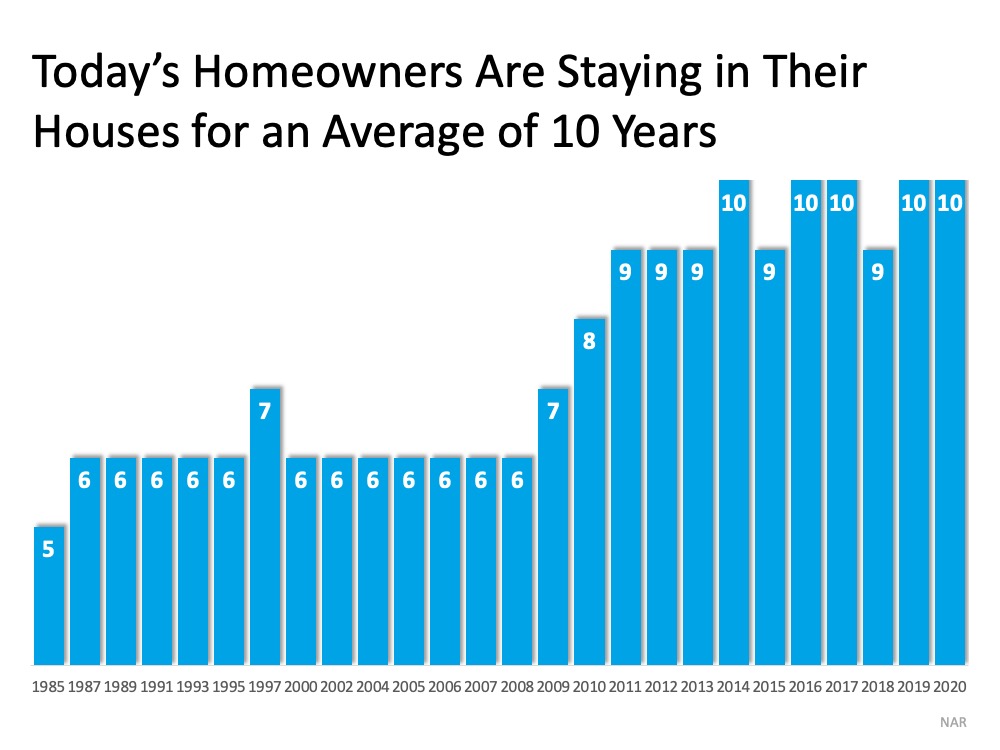

Today, homeowners are living in their houses for a longer period of time. Since 1985, the average time a homeowner owned their home, or their tenure, has increased from 5 to 10 years (See graph below): This is several years longer than what used to be the historical norm. The side effect, however, is when you stay in one place for so long, you may get even more emotionally attached to your space. If it’s the first home you purchased or the house where your children grew up, it very likely means something extra special to you. Every room has memories, and it’s hard to detach from that sentimental value.

This is several years longer than what used to be the historical norm. The side effect, however, is when you stay in one place for so long, you may get even more emotionally attached to your space. If it’s the first home you purchased or the house where your children grew up, it very likely means something extra special to you. Every room has memories, and it’s hard to detach from that sentimental value.

For some homeowners, that connection makes it even harder to separate the emotional value of the house from the fair market price. That’s why you need a real estate professional to help you with the negotiations along the way.

We’re generally quite proud of our décor and how we’ve customized our houses to make them our own unique homes. However, not all buyers will feel the same way about your design and personal touches. That’s why it’s so important to make sure you stage your house with the buyer in mind.

Buyers want to envision themselves in the space so it truly feels like it could be their own. They need to see themselves inside with their furniture and keepsakes – not your pictures and decorations. Stage, clean, and declutter so they can visualize their own dreams as they walk through each room. A real estate professional can help you with tips to get your home ready to stage and sell.

Today’s sellers’ market might be your best chance to make a move. If you’re considering selling your house, let’s connect today so you have the expert guidance you need to navigate through the process and prioritize these key elements.

Source: KCM

![Americans Choose Real Estate as the Best Investment [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2021/05/20143902/20210521-KCM-Share-549x300.png)

![Americans Choose Real Estate as the Best Investment [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2021/05/20143856/20210521-MEM.png)

Source: KCM

The level of equity homeowners have is at an all-time high. According to the U.S. Census, over 38% of owner-occupied homes are owned free and clear, meaning they don’t have a mortgage. Those with a mortgage are seeing their equity skyrocket too. Every time real estate values increase, homeowners get a dollar-for-dollar gain in their home equity.

According to the first-quarter 2021 U.S. Home Equity Report from ATTOM Data Solutions:

“17.8 million residential properties in the United States were considered equity-rich, meaning that the combined estimated amount of loans secured by those properties was 50 percent or less of their estimated market value.

The count of equity-rich properties in the first quarter of 2021 represented 31.9 percent, or about one in three, of the 55.8 million mortgaged homes in the United States. That was up from 30.2 percent in the fourth quarter of 2020, 28.3 percent in the third quarter and 26.5 percent in the first quarter of 2020.”

This surge in home equity has given most homeowners the opportunity to use that equity in one of two ways:

Let’s break down the possibilities.

An abundance of equity and record-low mortgage rates can make refinancing a home very easy. Some homeowners choose to refinance so they can lower their payments. Others convert a portion of the equity to cash while keeping their monthly payment the same.

There are many homeowners who could take advantage of lower rates and higher levels of equity, but they haven’t yet. According to an Economic & Housing Research Note from earlier this month, there were over five million homeowners with a loan funded by Freddie Mac who would benefit by refinancing their loan. As of January 2021, there were:

With mortgage rates currently hovering around 3%, any of these homeowners would benefit from refinancing. They could lower their payments by hundreds of dollars per month or cash out large sums of equity while keeping their monthly payment the same.

If a homeowner has a $200,000 fixed-rate mortgage with a 6% interest rate and refinances that loan to a 3% interest rate, their monthly mortgage payment (principal and interest) will go from $1,199 per month to $843 per month – a savings of $356 a month, or $4,272 each year.

On the other hand, if they keep their mortgage payment the same, they could cash out a significant amount of their equity.

The past year prompted many households to redefine what a dream home really means, and it’s something different to everyone. Those who have a high mortgage rate could use their equity as a down payment and perhaps buy their next home without significantly raising their mortgage payment.

Suppose a person bought a house for $216,000 at the height of the market in 2006. (The median home price in May of 2006). If they put 10% down and took out a mortgage of $194,400 at 6.41% (the average rate in 2006), the monthly mortgage payment (principal and interest) would have been $1,217.

According to the National Association of Realtors (NAR), a typical single-family home has grown in value by approximately $150,000 over the last fifteen years. That means the $216,000 house would be worth about $366,000 today.

After deducting selling expenses, they would be left with about $130,000 ($150,000 minus approximately $20,000 in selling expenses).

A seller could take that equity and use it as a down payment on a new house. Let’s assume they purchased a home for $450,000 (roughly $80,000 more than the value of their current home). If they put the $130,000 down, they could take out a mortgage of $320,000 with a 3% interest rate. The monthly mortgage payment (principal and interest) would be $1,349. Therefore, they could buy a home worth $80,000 more than the one they have today and only spend an extra $132 per month.

Whether you’re refinancing your house or moving to a new home, your current mortgage rate and your level of equity are crucial in your decision-making process. Look at your mortgage documentation to find out your interest rate, and then let’s connect to determine the potential equity in your home. You may be surprised by the opportunities you have.

Source: KCM

One of the biggest questions in real estate today is, “When will sellers return to the housing market?” An ongoing shortage of home supply has created a hyper-competitive environment for hopeful buyers, leading to the ultimate sellers’ market. However, as the economy continues to improve and more people get vaccinated, more sellers may finally be in sight.

The Home Purchase Sentiment Index (HPSI) by Fannie Mae recently noted the percentage of consumer respondents who say it’s a good time to sell a home increased from 61% to 67%. Doug Duncan, Senior Vice President and Chief Economist at Fannie Mae, indicates:

“Consumer positivity regarding home-selling conditions nearly matched its all-time high.” (See graph below):

Fannie Mae isn’t the only expert group noticing a rise in the percentage of people thinking about selling. George Ratiu, Senior Economist at realtor.com, shares:

Fannie Mae isn’t the only expert group noticing a rise in the percentage of people thinking about selling. George Ratiu, Senior Economist at realtor.com, shares:

“The results of a realtor.com survey . . . showed that one-in-ten homeowners plans to sell this year, with 63 percent of those, looking to list in the next 6 months. Just as encouragingly, close to two-thirds of sellers plan to sell their homes at prices under $350,000, which would offer a tremendous boost to affordable housing for first-time buyers.”

If you’re considering selling your house, don’t wait for more competition to pop up in your neighborhood. Let’s connect today to explore the benefits of selling your house now before more homes come to the market.

Source: KCM

Last month, in a post on the Liberty Street Economics blog, the Federal Reserve Bank of New York noted that Americans believe buying a home is definitely or probably a better investment than buying stocks. Last week, a Gallup Poll reaffirmed those findings.

In an article on the current real estate market, Gallup reports:

“Gallup usually finds that Americans regard real estate as the best long-term investment among several options — seeing it as superior to stocks, gold, savings accounts and bonds. This year, 41% choose real estate as the best investment, up from 35% a year ago, with stocks a distant second.”

Here’s the breakdown: The article goes on to say:

The article goes on to say:

“The 41% choosing real estate is the highest selecting any of the five investment options in the 11 years Gallup has asked this question.”

Some question American confidence in real estate as a good long-term investment right now. They fear that the build-up in home values may be mirroring what happened right before the housing crash a little more than a decade ago. However, according to Merrill Lynch, J.P. Morgan, Morgan Stanley, and Goldman Sachs, the current real estate market is strong and sustainable.

As Morgan Stanley explains to their clients in a recent Thoughts on the Market podcast:

“Unlike 15 years ago, the euphoria in today’s home prices comes down to the simple logic of supply and demand. And we at Morgan Stanley conclude that this time the sector is on a sustainably, sturdy foundation . . . . This robust demand and highly challenged supply, along with tight mortgage lending standards, may continue to bode well for home prices. Higher interest rates and post pandemic moves could likely slow the pace of appreciation, but the upward trajectory remains very much on course.”

America’s belief in the long-term investment value of homeownership has been, is, and will always be, very strong.

Source: KCM

When buying a home, it’s important to have a budget and make sure you plan ahead for certain homebuying expenses. Saving for a down payment is the main cost that comes to mind for many, but budgeting for the closing costs required to get a mortgage is just as important.

According to Trulia:

“When you close on a home, a number of fees are due. They typically range from 2% to 5% of the total cost of the home, and can include title insurance, origination fees, underwriting fees, document preparation fees, and more.”

For example, for someone buying a $300,000 home, they could potentially have between $6,000 and $15,000 in closing fees. If you’re in the market for a home above this price range, your closing costs could be greater. As mentioned above, closing costs are typically between 2% and 5% of your purchase price.

Trulia gives more great advice, explaining:

“There will be lots of paperwork in front of you on closing day, and not enough time to read them all. Work closely with your real estate agent, lender, and attorney, if you have one, to get all the documents you need ahead of time.

The most important thing to read is the closing disclosure, which shows your loan terms, final closing costs, and any outstanding fees. You’ll get this form about three days before closing since, once you (the borrower) sign it, there’s a three-day waiting period before you can sign the mortgage loan docs. If you have any questions about the numbers or what any of the mortgage terms mean, this is the time to ask—your real estate agent is a great resource for getting you all the answers you need.”

As home prices are rising and more buyers are finding themselves competing in bidding wars, it’s more important than ever to make sure your plan includes budgeting for closing costs. Let’s connect to be sure you have everything you need to land your dream home.

Source: KCM