There has been a great amount written on millennials and their impact on the housing market. However, the headlines often contradict each other. Some claim this generation is becoming the largest share of first-time home buyers, while others claim millennials don’t want to own a home, blaming them for the dip in homeownership rate.

While it is true that millennials have achieved milestones like getting married, having kids, and buying homes later in life than their parents and grandparents did, they are not solely to blame for today’s housing market trends.

Freddie Mac’s Insight Report explored the impact of the Silent and Baby Boomer Generations on the housing market.

If millennials are unable to find a home to buy at a young age like their predecessors, then who is living in those homes?

The answer: Seniors born after 1931 are staying in their homes longer than previous generations, instead choosing to “age in place.”

Freddie Mac found that,

“this trend accounts for about 1.6 million houses held back from the market through 2018, representing about one year’s typical supply of new construction, or more than half of the current shortfall of 2.5 million housing units estimated in December’s Insight.

Older Americans prefer to age in place because they are satisfied with their communities, their homes, and their quality of life.”

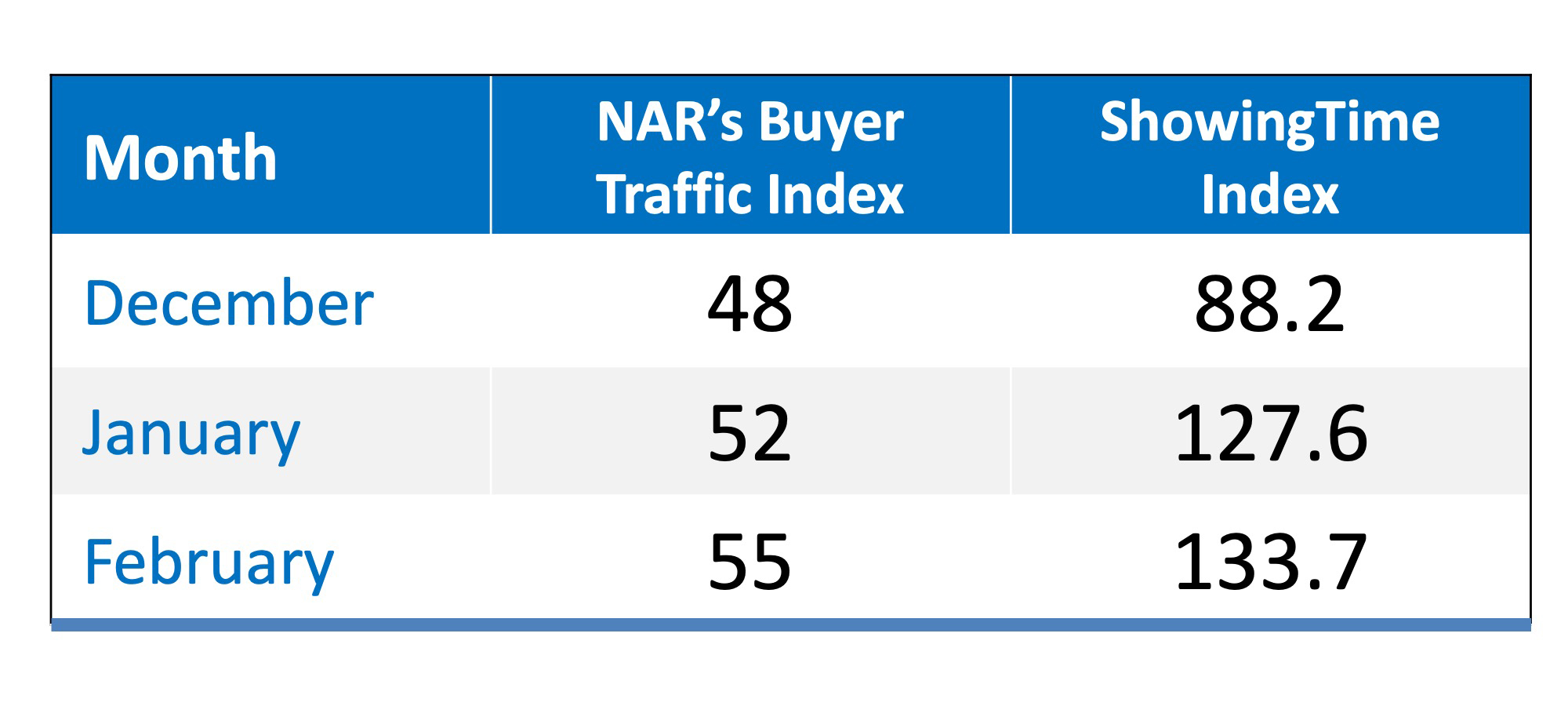

According to the National Association of Realtors, inventory of homes for sale is currently at a 3.5-month supply, which means that nationally we are in a seller’s market. A ‘normal’ housing market requires 6-7 months inventory, a level we have not achieved since August 2012.

“The most important fundamental in today’s housing market is the lack of houses for sale. This shortage has been identified as an important barrier to young adults buying their first homes.”

Bottom Line

If you are one of the many seniors who desires to retire in the same area you’ve always lived, you’re not alone. Will your current house fit your needs throughout retirement? If you have any questions about demand for your house, let’s get together to discuss the opportunities available today!

Source: KCM

![Existing Home Sales Slow to Start Spring [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2019/04/23164814/20190426-Share-KCM-549x300.jpg)

![Existing Home Sales Slow to Start Spring [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2019/04/23164805/20190426-EHS-Report-ENG-MEM.jpg)

![5 Reasons Why Millennials Buy a Home [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2019/04/09111636/20190419-Share-KCM-549x300.jpg)

![5 Reasons Why Millennials Buy a Home [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2019/04/09111414/Millennials-Choose-to-Buy-ENG-MEM1.jpg)