More Contracts Are Falling Through. Here’s How To Get Ahead.

When you sell a house, the last thing you want is for the deal to fall apart right before closing. […]

When you sell a house, the last thing you want is for the deal to fall apart right before closing. […]

Mortgage rates are still a hot topic – and for good reason. After the most recent jobs report came out

If you’ve been skipping over newly built homes in your search, you might be doing so based on outdated assumptions.

Some Highlights Now that there are more homes for sale, buyers have more options. And sellers need to be more

Believe it or not, there are clear signs buyer interest is heating up again. Let’s talk about what’s really going

Cutting out the agent might seem like a smart way to save when you sell your house. But here’s the

Selling your house without an agent as a “For Sale by Owner” (FSBO) may be something you’ve considered. But you

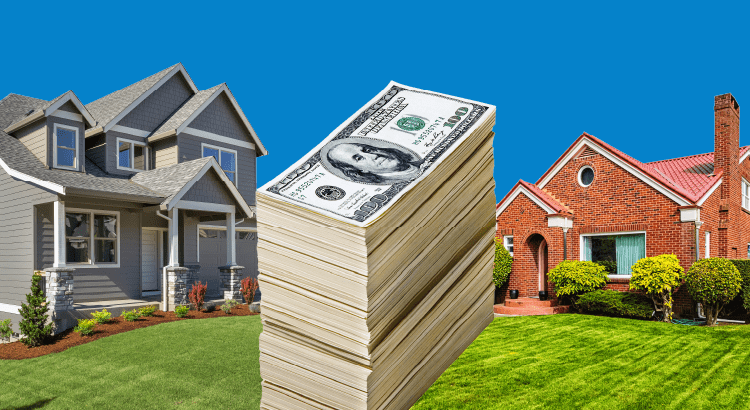

Some Highlights Have you been holding off on downsizing? If so, you should know your equity could make your move possible.

When your house doesn’t sell, it doesn’t just feel frustrating – it feels personal. You put time, money, and emotional

After years of it feeling almost impossible to find a home you want to buy, things are changing for the